Why Build Business Credit: Complete Guide for Entrepreneurs

Did you know over 60 percent of small businesses get denied funding due to weak business credit? This silent scorecard shapes whether your company can secure loans, snag better deals with suppliers, or even qualify for lower insurance rates. Building strong business credit creates a clear line between your company’s finances and your personal financial health, putting you in control and ready to seize new growth opportunities.

Table of Contents

- What Business Credit Really Means

- Key Benefits of Building Business Credit

- Business Credit vs. Personal Credit Differences

- Steps to Start Establishing Business Credit

- Potential Risks and Cost Considerations

Key Takeaways

| Point | Details |

|---|---|

| Establishing Business Credit | Business credit is crucial for a company’s financial reputation, allowing businesses to operate independently from personal credit. |

| Benefits of Strong Business Credit | A solid business credit score enhances financing options, lowers borrowing costs, and improves supplier relationships. |

| Differences from Personal Credit | Business credit is tied to the company entity, offering legal separation that protects personal assets and affects business financing. |

| Strategic Building Steps | Establish business credit by registering legally, maintaining a dedicated account, and responsibly managing debts for sustained growth. |

What Business Credit Really Means

Business credit is like a financial reputation for your company - separate from your personal credit score but just as important. According to Experian, business credit refers to a company’s ability to borrow money or access goods and services under its own name, based entirely on the business’s financial track record.

Think of business credit as your company’s financial passport. Just like how your personal credit determines your loan eligibility, business credit tells lenders and vendors how trustworthy your business is. Unlike personal credit, which follows you individually, business credit is tied specifically to your business entity. This means your business can build its own financial credibility independent of your personal financial history.

How Business Credit Works

Business credit operates through a unique system of evaluation. Experian explains that business credit bureaus track and score your company’s financial behaviors. Key factors that impact your business credit include:

- Payment history with vendors and suppliers

- Credit utilization rates

- Length of business operational history

- Past financial performance

- Legal and financial structure of your business

Building strong business credit isn’t just about getting loans. It’s about establishing financial credibility that can open doors to better financing, lower interest rates, and more favorable terms with vendors. For single mothers and entrepreneurs looking to grow their businesses, understanding and strategically developing business credit can be a game-changing financial strategy.

The beauty of business credit is that it creates a separate financial identity for your venture. This means your personal credit score won’t be directly impacted by your business’s financial moves, providing an added layer of financial protection and opportunity for growth.

Key Benefits of Building Business Credit

Building business credit isn’t just a financial formality - it’s a strategic move that can transform your entrepreneurial journey. Chase highlights that business credit fundamentally enhances access to financing options while helping entrepreneurs separate personal and business finances.

The advantages of robust business credit extend far beyond simple loan accessibility. According to FNBI, a strong business credit score can unlock multiple financial advantages that directly impact your bottom line. These benefits aren’t just theoretical - they’re practical advantages that can help single mothers and entrepreneurs scale their businesses more effectively.

Financial Advantages of Strong Business Credit

Here’s what building solid business credit can mean for your venture:

- Improved Financing Options: Better loan terms and higher credit limits

- Lower Borrowing Costs: Reduced interest rates on business loans

- Supplier Relationships: More favorable payment terms and credit arrangements

- Insurance Benefits: Potentially lower insurance premiums

- Business Credibility: Enhanced reputation with lenders and partners

The most powerful aspect of building business credit is creating financial independence. By establishing a separate credit profile for your business, you’re not just protecting your personal credit - you’re creating a foundation for sustainable growth. This means your business can access resources, negotiate better terms, and expand opportunities without risking your personal financial health.

For single mothers and entrepreneurs, business credit isn’t just a number. It’s a pathway to financial empowerment, offering the flexibility and resources needed to turn entrepreneurial dreams into tangible success. Your business credit score becomes a testament to your professionalism, reliability, and potential for future growth.

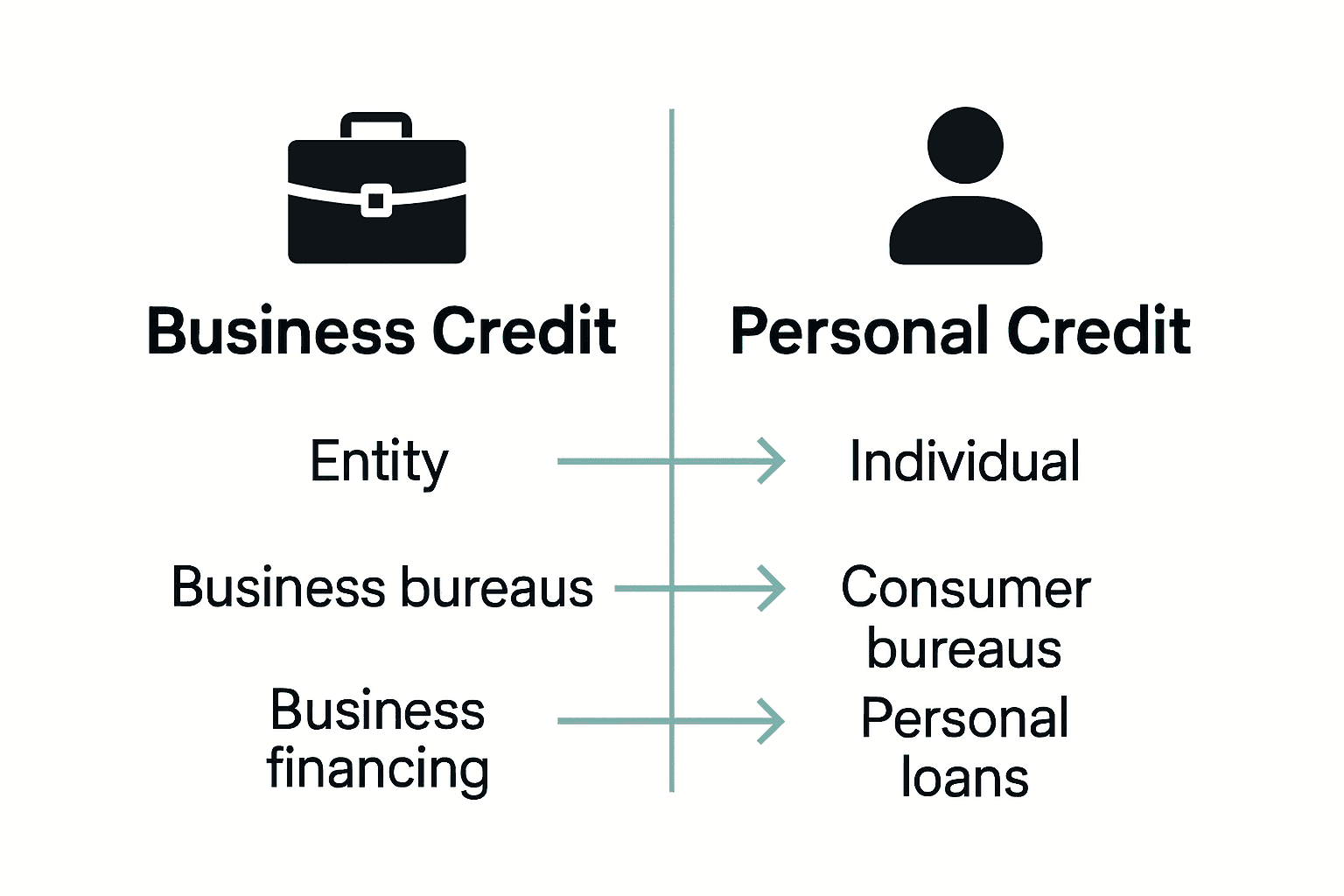

Business Credit vs. Personal Credit Differences

Understanding the distinction between business and personal credit is crucial for entrepreneurs seeking financial independence. Experian explains that business credit is fundamentally different from personal credit, being tied specifically to a company’s financial activities and evaluated through an entirely separate lens.

While personal credit follows you as an individual, tracking your personal financial decisions and borrowing history, business credit creates a unique financial identity for your venture. According to Wikipedia, business credit cards are specifically issued under a registered business name and intended exclusively for business expenses - creating a clear separation from personal financial transactions.

Key Differences Explained

Here’s a breakdown of the critical distinctions between business and personal credit:

Here’s a comparison of business credit and personal credit:

| Feature | Business Credit | Personal Credit |

|---|---|---|

| Linked To | Business entity | Individual |

| Evaluation Criteria | Revenue Operational history Vendor payments |

Income Personal debt Payment history |

| Impact | Business financing options Vendor terms |

Personal loans and credit cards |

| Reporting Agencies | Business credit bureaus | Consumer credit bureaus |

| Legal Separation | Protects personal assets | Directly tied to personal assets |

| Card Usage | For business expenses | For personal expenses |

-

Evaluation Criteria:

- Personal Credit: Based on individual income, debt-to-income ratio, and personal payment history

- Business Credit: Evaluated on business revenue, years of operation, payment history with vendors

-

Legal Implications:

- Personal Credit: Directly impacts individual borrowing capabilities

- Business Credit: Protects personal assets and provides separate financial standing

-

Reporting Mechanisms:

- Personal Credit: Reported by consumer credit bureaus

- Business Credit: Tracked by specialized business credit reporting agencies

The most significant advantage of maintaining separate business credit is financial protection. By building a distinct credit profile for your business, you’re creating a shield that prevents your personal financial health from being directly impacted by business financial activities. This separation is especially critical for single mothers and entrepreneurs who need to maintain personal financial stability while growing their ventures.

Think of business credit as your company’s financial reputation - a dynamic, evolving profile that demonstrates your business’s reliability, growth potential, and financial maturity. It’s not just about numbers, but about building a credible financial story that opens doors to opportunities, resources, and potential partnerships.

Steps to Start Establishing Business Credit

Establishing business credit is a strategic journey that requires careful planning and intentional financial management. Chase highlights that business credit fundamentally involves obtaining credit specifically in your business’s name and responsibly managing business debts to build a solid financial foundation.

For single mothers and entrepreneurs, the path to building business credit might seem complex, but it’s entirely achievable with a structured approach. The key is to create a clear separation between personal and business finances, demonstrating your business’s financial reliability and potential to lenders and credit bureaus.

Practical Steps to Build Business Credit

Here’s a comprehensive roadmap for establishing your business credit:

-

Register Your Business Legally

- Choose a business structure (LLC, Corporation)

- Obtain an Employer Identification Number (EIN)

- Create a dedicated business bank account

-

Establish Business Credit Foundations

- Get a business phone number

- Create a professional business address

- Register your business with business credit bureaus

-

Obtain Initial Credit Lines

- Apply for a business credit card

- Open vendor credit accounts

- Consider small business store credit lines

-

Build Credit Responsibly

- Always pay bills on time

- Keep credit utilization low (under 30%)

- Maintain consistent financial records

The most powerful strategy is patience and consistency. Building business credit isn’t an overnight process - it’s about creating a track record of financial responsibility. Each on-time payment, each responsible credit decision builds your business’s financial reputation, opening doors to larger opportunities and more favorable financing terms.

Remember, your business credit is more than just a score. It’s a testament to your entrepreneurial journey, reflecting your commitment, reliability, and potential for growth. By methodically building your business credit, you’re not just securing financing - you’re creating a financial foundation that can transform your entrepreneurial dreams into sustainable success.

Potential Risks and Cost Considerations

Building business credit is a double-edged sword that requires strategic navigation. FNBI warns that while establishing business credit offers significant benefits, it also demands careful management to prevent potential financial strain and over-leveraging.

Single mothers and entrepreneurs must approach business credit with a balanced perspective, understanding both its opportunities and potential pitfalls. Chase emphasizes that mismanagement of business credit can lead to serious financial challenges, including higher interest rates and reduced access to future financing options.

Critical Financial Risks to Monitor

Key risks and potential cost considerations include:

-

Debt Accumulation:

- Risk of taking on more credit than your business can manage

- Potential for high-interest debt spirals

- Importance of maintaining strict credit discipline

-

Credit Score Impact:

- Missed payments can significantly damage business credit

- Negative marks can persist for years

- Potential limitations on future borrowing capabilities

-

Hidden Costs:

- Annual fees for business credit cards

- Transaction fees and interest charges

- Potential penalties for late payments

The most critical strategy is maintaining a proactive and disciplined approach to financial management. Every credit decision should be carefully evaluated against your business’s current financial capacity and long-term growth objectives. This means creating robust financial planning processes, maintaining detailed records, and consistently monitoring your business’s financial health.

Remember, business credit is a tool - not a lifeline. The goal is strategic financial empowerment, not creating additional financial stress. By understanding potential risks, implementing careful management strategies, and making informed decisions, you can leverage business credit as a powerful mechanism for sustainable business growth.

Take Charge of Your Business Credit and Unlock New Opportunities

Building strong business credit is essential for entrepreneurs who want to create financial independence while protecting personal assets. The article highlights how business credit opens doors to better loans, lower interest rates, and stronger vendor relationships — all crucial for single mothers and ambitious women eager to grow their businesses without risking personal financial stability. Yet navigating these steps can feel overwhelming without the right guidance.

If you are ready to turn the concept of business credit into a practical tool for growth, visit Prosperual to access resources designed especially for entrepreneurs like you. Our flagship program, “Thrive and Prosper,” offers clear strategies for separating your personal and business finances, building credit responsibly, and leveraging your business credit to create sustainable income streams. Don’t wait to secure the financial future you and your family deserve. Start your journey today by exploring Prosperual’s empowering solutions and learn how to confidently build the business credit that fuels your dream.

Frequently Asked Questions

What is business credit and why is it important?

Business credit refers to a company’s ability to borrow money or access goods and services based on its own financial history, separate from the owner’s personal credit. It is essential as it enhances access to financing options and helps establish a solid financial reputation for the business.

How can I start building business credit?

To start building business credit, you should legally register your business, obtain an Employer Identification Number (EIN), create a dedicated business bank account, and establish credit foundations like getting a business phone number and professional business address. Then, apply for business credit cards and vendor accounts to build a credit history.

What are the key benefits of maintaining strong business credit?

Strong business credit improves financing options, lowers borrowing costs, enhances supplier relationships, potentially reduces insurance premiums, and builds business credibility with lenders and partners, facilitating easier access to resources and better terms.

What are the risks associated with building business credit?

The risks of building business credit include the potential for debt accumulation, negative impacts on credit scores due to missed payments, hidden costs such as annual fees and transaction charges, and over-leveraging which can strain business finances. Maintaining strict financial management is crucial to mitigate these risks.

Recommended

- What Is E-Commerce Business? Complete Guide – Prosperual

- Why Choose Entrepreneurship: Complete Guide for Moms – Prosperual

- Financial Planning for Single Moms: Build Wealth Step-by-Step – Prosperual

- Best Business Startup Tools for Mothers – 2025 Comparison – Prosperual

- Understanding Blogging for Business: A Key to Growth

- Crédit professionnel